Subscribe to our newsletter

Complete the form below and we will send you our latest news and insights.

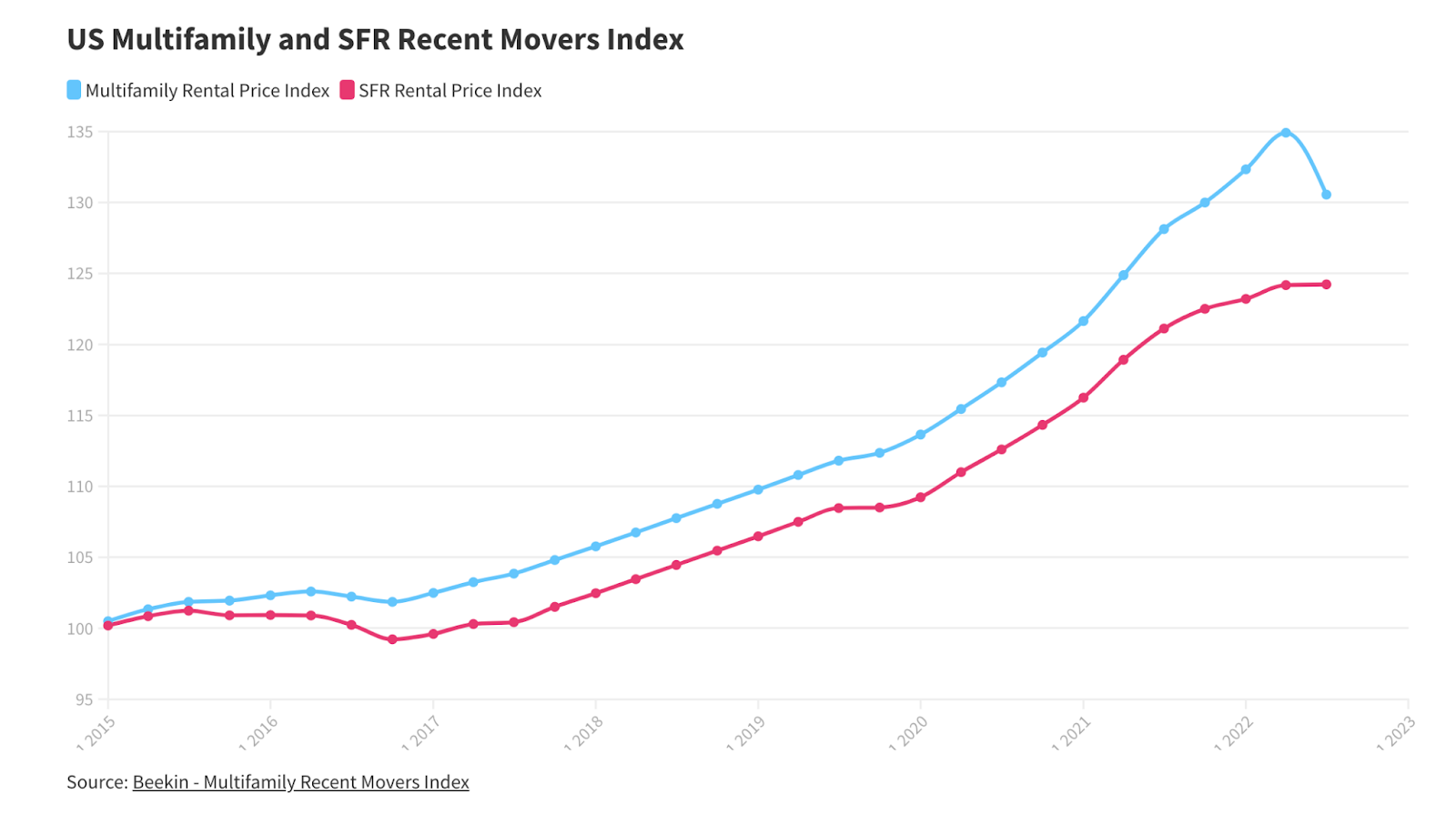

While a lot of attention has gone to existing asset classes such as multifamily, single family rentals and short term rentals, not a lot is understood about build to rent, which is an emerging asset class with strong fundamentals, and few existing assets that are stable and income producing. Hence very little is known about Build to Rent (BTR) in reality.

This comes on the back of late-2022 news of institutional funds such as JP Morgan, and JLL Income property trust, striking joint venture deals in single family to invest around $500 MM in BTR as well as scattered site single family. The inflation resistance was cited as a big focus around residential real estate and SFR and BTR.

In the end, institutional landlords produce vital housing which is in short supply. With the rise in interest rates, home ownership is increasingly unaffordable for Americans, and quality rental housing can indeed fill the gap.

In a webinar organized by Beekin, 3 institutional investors who have invested in build to rent, talked about the state of transactions, underwriting process and performance of their existing BTR product.

Attracting over 100 pre-eminent participant, the webinar attracted a majority of institutional investors and developers, potentially looking for answers to underwriting and demand questions from 3 eminent operators and investors in BTR.

The panelists covered a few key key areas

Changes to underwriting due to interest rates

Homebuilders are increasingly looking to BTR operators to help them with products available for sale, as well as recent construction starts. Large discounts are being offered by both national and regional builders in order to transact.

With interest rates rising, the loan to value on deals has fallen to make the mathematics work and transactions have paused. This is due to the environment of rising interest rates. Due to greater volatility, there are fewer deals done as the market is moving quite quickly.

Per Geoff, macroeconomically, the present value of future cash flows are worth less due to higher discount rates. That means that whereas in a (previous) low rate environment deals with first deliveries far off in the future (<3 years delivery) would converge in pricing on an asset that’s stabilized already. Now, no one will be paying top dollar for an asset that’s going to be stabilized in three years. Due to a risk premium expansion and a greater compensation demanded per unit of risk by the market, there is a a focus on core markets, fewer riskier projects will be undertaken.

“Long term, it’s going to drive up the cost of housing both on a rental perspective and purchasing a home. A year or two years in future, many of these builders that are slowing down are starting to stop construction or development. When the pendulum swings the other way, interest rates go down a little bit, that’s going to create even a smaller supply of housing, affordable housing. And it’s going to take us many years to recover. “

Bruce McNeilage, Founder and CEO Kinloch Partners

Horizontal multifamily is different to BTR which typically has more bedrooms. Premium for 4 over 3 bedrooms increased and more construction geared towards 4 rooms versus apartments which only have 1-2 bedrooms.

As demand for apartments is seeing a big dip, BTR is starting to perform similar to single family rentals. This is due to the tenant demographic who choose houses over apartments. BTR is under supplied in areas where tenants are demanding better quality product and hence it still earns a rent premium over single family whilst, representing the institutional premium of multifamily (over condos) but with the lower volatility in cashflow represented by single family homes.

‘Historically, build for rent tenants have a very high household income. It used to be $120,000 on average. I think now it’s pushing $130,000 average. And so if it’s just much stickier tenants,. But still for a single family rental compared to multifamily, you have a higher tenancy rate for build for rent it’s about five and a half year average resident tenure. So you’re really not dealing with the risk of having to find a new tenant every single year.

Audrey Carlson, Director of Asset Optimization and Design, SVN

As transactions have slowed down and deals are harder to underwrite, all 3 players commented on the need to be more forensic around market selection, rent premiums and configuration of product while building BTR communities. They also averred that their consumption of data would increase in 2023 as they believed in data to make better decisions through this crisis

‘(BTR) is a highly inefficient market. It’s both highly inefficient and one where there’s an enormous amount of data out there. A lot of these nuances such as the type of tenant , location, are not appropriately priced in. Appropriately looking at the data and harvesting that data in order to make decisions is, I think, crucial to make sure that you’re able to truly weather it down’

Geoffrey Kristof – Head of Single-Family Rental, APL Group